When "Clarity" Becomes Capture - The Blockchain Boys have responded

For years, the crypto industry begged for a map. We asked for "Clarity" so we could build without the shadow of enforcement-by-whim. On January 15, 2026, the Senate Banking Committee finally handed us that map—but as Shanaka Anslem Perera brilliantly exposes, it was not a guide to the future. It was a deed of ownership for the past.

The Clarity Act has been revealed as the ultimate extraction mechanism. By delaying the bill after Brian Armstrong’s 11th-hour opposition, the Senate has not just paused a debate; they have confirmed that the "Great Re-Centering" has hit a $6.6 trillion wall of banking lobbyists.

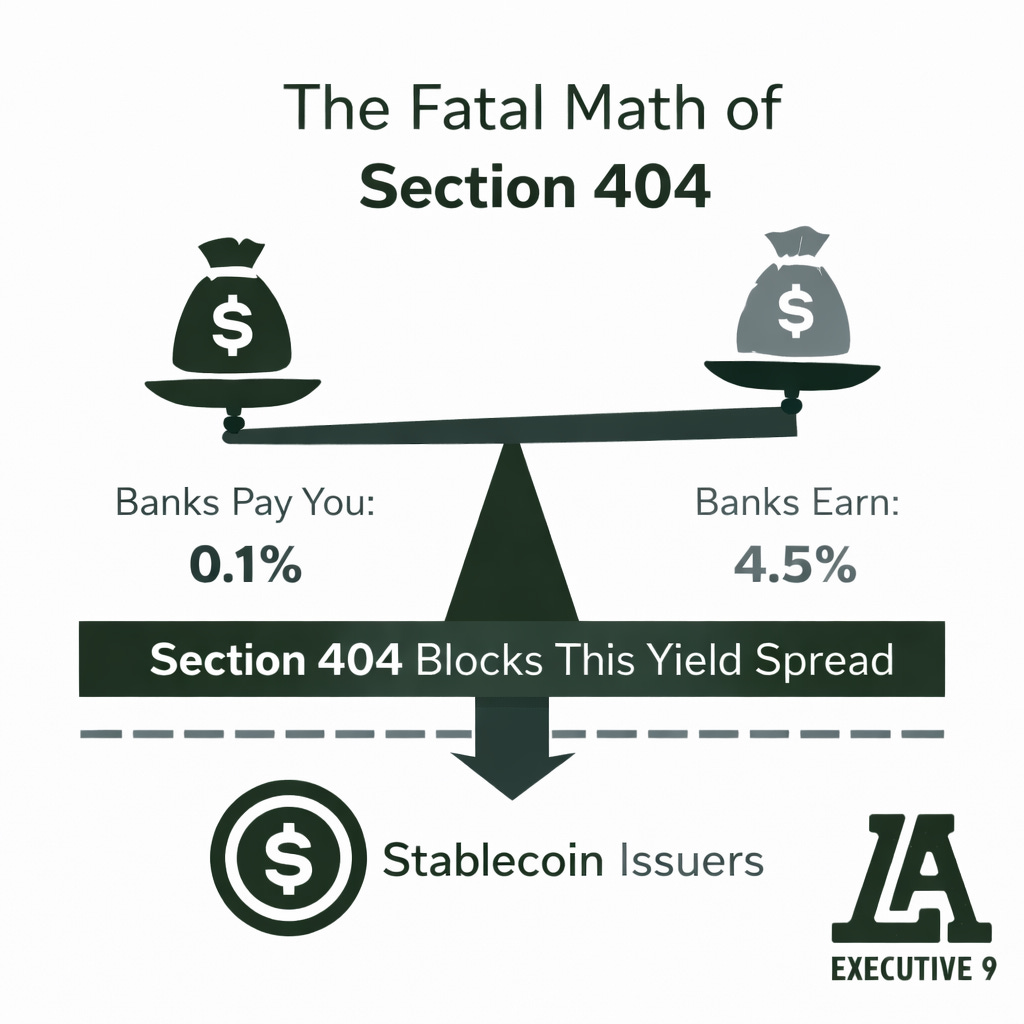

The Fatal Math of Section 404

Perera’s "Yield Apartheid" isn't hyperbole—it’s arithmetic.

The Spread: Banks pay you 0.1%. They take your deposits and buy Treasuries earning 4.5%. They pocket the 4.4% difference.

The Disruptor: Stablecoin issuers want to give that 4.4% back to you.

The "Clarity" Solution: Section 404 of the Act effectively makes it illegal for stablecoin issuers, exchanges, or partners to pass that yield to the consumer. This insulates current intermediaries, like banks.

In The Polymath terms, this is the transition from Experimentation (stablecoins proving they can provide better yield) to Extraction (banks using the law to ensure they are the only ones allowed to profit from your "idle" cash).

Brian Armstrong’s "No Bill > Bad Bill" Moment

Coinbase’s sudden withdrawal of support is a seismic shift in U.S. crypto policy. After spending millions to get pro-crypto candidates elected in 2024, Armstrong realized the industry was being "Dodd-Franked."

The Betrayal: The industry funded the candidates; the banking associations (all 53 of them) wrote the fine print.

The Realization: Regulatory capture is so brazen that the bill allows "rewards" (loyalty points) but bans "yield" (actual money). It treats the American citizen as a child who can be paid in stickers, while the banks keep the gold.

The Geopolitical Pivot: America vs. China

While the U.S. Senate bickers over how to protect a 20th-century banking model, the rest of the world is moving into 2026.

China’s Move: On December 29, Beijing made the e-CNY (digital yuan) interest-bearing.

The Leadership Gap: We are currently witnessing a "Regulatory Suicide." By banning yield, the U.S. is incentivizing capital to flee to offshore, yield-bearing digital assets. We are ceding the "borderless movement of value" to our competitors in the name of protecting community bank balance sheets.

What This Means for U.S. Leadership

This delay is not a sign of a functioning democracy; it is a sign of a system in shock. The Kansas City Fed’s warning that competitive stablecoins could drain 25% of bank deposits is not a "risk" to the economy—it is a market signal that the banking model is obsolete.

If the U.S. government chooses to "save" the banks by "banning" the math of stablecoins, they are not protecting the consumer. They are enforcing an Economic Apartheid where the wealthy can access institutional yield, but the marginalized communities in the South—who I have argued need these "Pillars of Progress"—are legally barred from the same returns.

Is The Re-Centering Postponed?

The "Great Re-Centering" is inevitable, but the Clarity Act proves that the gatekeepers will not go quietly. They have stopped being "intermediaries" and have become "insurgents" against their own customers. The Clarity Act shows us what happens when the "Old Guard" tries to buy the laws of the future.

The question for 2026 is no longer "When will we get regulation?" but "Who is the regulation actually for?"